What To Do To Get Financially Sound Home Mortgages

Article by-Adcock GottliebWhen first seeking out a mortgage, many people feel overwhelmed. There are so many different lenders to consider, and their rates all seem so vastly different. How can one compare them all without going mad? The tips in this article will help you determine which mortgage is the right one for you.

When you struggle with refinancing, don't give up. New programs (HARP) are in place to help homeowners out in this exact situation, no matter how imbalanced their mortgage and home value seems to be. Consider having a conversation with your mortgage lender to see if you qualify. If your lender is still not willing to work with you, find another one who will.

Be prepared before obtaining your mortgage. Every lender will request certain documents when applying for a mortgage. Do not wait until they ask for it. Have the documents ready when you enter their office. You should have your last two pay stubs, bank statements, income-tax returns, and W-2s. Save all of these documents and any others that the lender needs in an electronic format, so that you are able to easily resend them if they get lost.

Get a pre-approval letter for your mortgage loan. A pre-approved mortgage loan normally makes the entire process move along more smoothly. It also helps because you know how much you can afford to spend. Your pre-approval letter will also include the interest rate you will be paying so you will have a good idea what your monthly payment will be before you make an offer.

Be prepared before obtaining your mortgage. Every lender will request certain documents when applying for a mortgage. Do not wait until they ask for it. Have the documents ready when you enter their office. You should have your last two pay stubs, bank statements, income-tax returns, and W-2s. Save all of these documents and any others that the lender needs in an electronic format, so that you are able to easily resend them if they get lost.

Learn of recent property tax history on any home you're thinking of buying. You should understand just how much your property taxes will be before buying a home. The tax assessor may consider your property to be more valuable than you expect, leading to an unpleasant surprise at tax time.

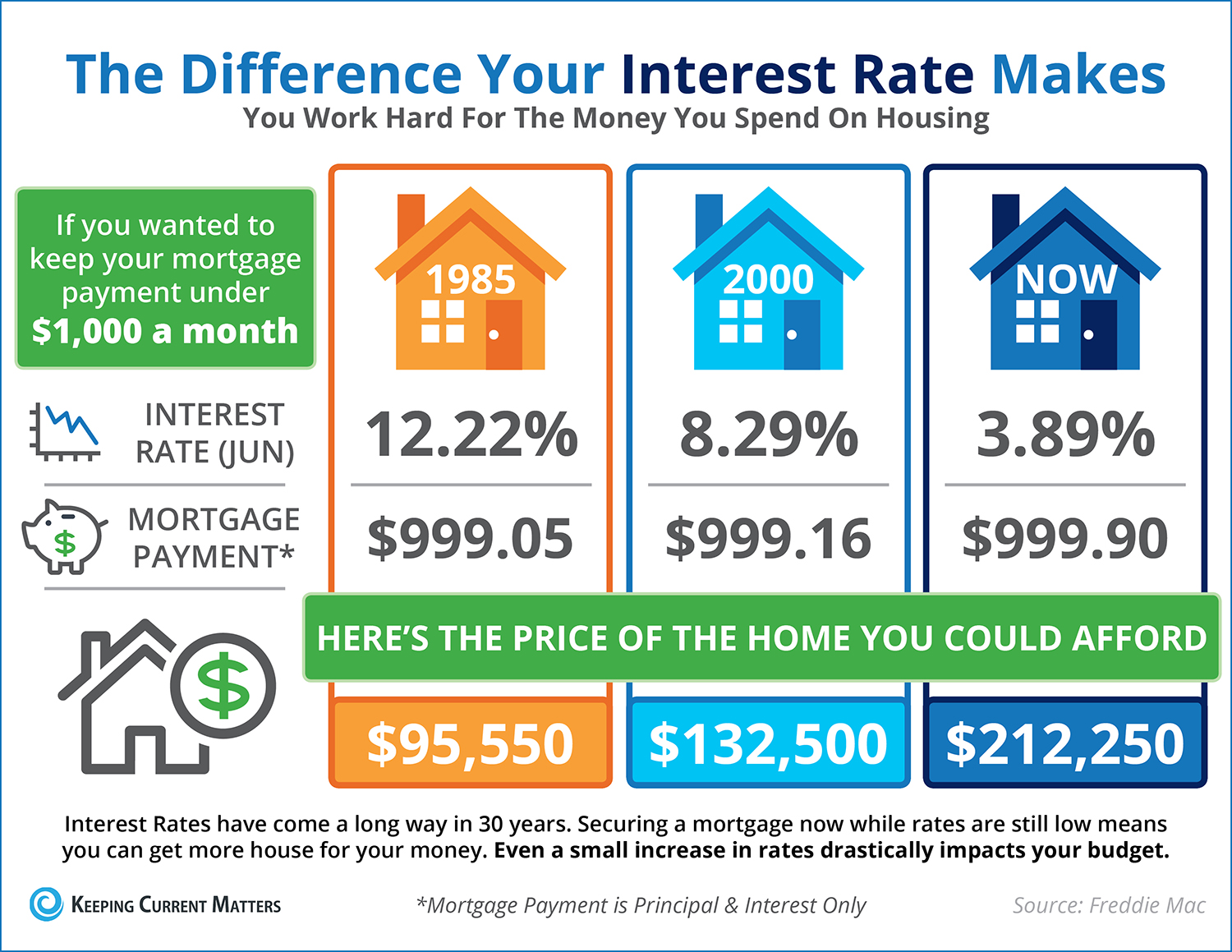

Do not sign a home mortgage contract before you have determined that there is no doubt that you will be able to afford the payments. Just because get redirected here approves you for a loan does not mean that you could really endure it financially. First do the math so that you know that you will be able to keep the home that you buy.

Define your terms before you apply for the mortgage, not only will this help show your lender you are equipped to handle the mortgage, but also for your own budget. Buy a house that fits into your budget. No matter how great a new home is, if it leaves you strapped, trouble is bound to ensue.

If you are looking to buy any big ticket items, make sure that you wait until your loan has been closed. Buying large items may give the lender the idea that you are irresponsible and/or overextending yourself and they may worry about your ability to pay them back the money you are trying to borrow.

You can request for the seller to pay for certain closing costs. For example, a seller can pay either a percentage of the closing cost or for certain services. Many times the seller is responsible for paying for a termite inspection along with a survey and appraisal of the property.

Some financial institutions allow you to make extra payments during the course of the mortgage to reduce the total amount of interest paid. This can also be set up by the mortgage holder on a biweekly payment plan. Since there is often a charge for this service, just make an extra payment each year to gain the same advantage.

Avoid paying Lender's Mortgage Insurance (LMI), by giving 20 percent or more down payment when financing a mortgage. If you borrow more than 80 percent of your home's value, the lender will require you to obtain LMI. LMI protects the lender for any default payment on the loan. It is usually a percentage of your loan's value and can be quite expensive.

Never assume that a mortgage is going to just get a home for you outright. Most lenders are going to require you to chip in a down payment. Depending on the lender, this can be anywhere from 5 percent to a full fifth of the total home value. Make sure you have this saved up.

Ensure that your mortgage does not have any prepayment penalties associated with it. A prepayment penalty is a charge that is incurred when you pay off a mortgage early. By avoiding these fees, you can save yourself thousands. Most of today's loans do not have prepayment penalties; however, some still do exist.

Negotiate a better interest rate on your mortgage by bringing your other assets to the potential lending bank. Transferring your savings accounts, checking accounts and money market accounts to the lenders bank can result in a lower interest rate. A bank may also be more willing to make a loan to a customer of their bank.

Check your mortgage broker out through your local Better Business Bureau. Brokers who are predatory will resort to tricks to get you to pay higher fees to earn themselves a higher commission. Avoid lenders who charge excessive points and high fees.

Contrary to popular belief, there are plenty of lenders out there who will loan to you. So you need to shop around with your loan options. Never jump at the first opportunity you find. https://business.chase.com/resources/grow/putting-a-business-line-of-credit-to-work will leave you paying far too much and will leave you obligated to a loan whose terms are not favorable to you.

How flexible is the payment schedule being offered to you? With greater flexibility comes the ability to pay off your mortgage more quickly, but it may also include higher interest rates. Consider how much you will spend over the entire life of the mortgage as you compare your options.

Never choose a home mortgage from a company that asks you to do unscrupulous things. If a rep is asking you to claim more than you make to secure the mortgage, it's not a good sign that your mortgage is in good hands. Walk away from these deals as quickly as you can.

You now have a plan of action you can take to ensure that the mortgage you find is the perfect choice. Just use everything you've learned here today to make your process a simple one. The sooner you are into your home, the better, so get down to work right away!